Yes. Insurance for a single day is available.

Unpacking AAA Car Rental Insurance: What’s Covered?

PUBLISHED ON Jun, 05 2023

UPDATED ON Mar, 05 2024

The American Automobile Association (AAA), founded in 1902, is a federation of motor clubs throughout North America, renowned for its roadside assistance programs. However, AAA’s offerings extend well beyond roadside services, and it has also made a name for itself as a comprehensive insurance provider.

AAA’s insurance arm provides members with a wide range of insurance options including auto, home, life, and more. AAA auto insurance, available to members, offers numerous collision insurance coverage options designed to protect policyholders financially in the event of an accident or other vehicle-related incidents.

Understanding the nuances of your auto insurance policy can be crucial, particularly when it comes to coverage for rental cars. The American Automobile Association (AAA) is a well-known provider of auto insurance, offering a wide array of coverage options. This article will explore AAA’s rental car insurance policies, how they apply, and the process of filing a claim if needed. We’ll provide a comprehensive view of AAA’s collision coverage, allowing you to make informed decisions when it comes to your insurance needs and ensuring you’re well-prepared for any rental car contingencies.

Rental Car Coverage: The Basics

What rental car coverage generally includes

Rental car insurance typically includes several types of coverage. Here’s a general breakdown:

- Collision Damage Waiver (CDW)/Loss Damage Waiver (LDW): This is not traditional insurance, but rather a waiver that says the rental car company will not come after you for collision costs in case the rental car is damaged or stolen. There may be exclusions, so it’s important to read the terms and conditions.

- Supplemental Liability Protection (SLP): This provides extra liability protection for costs associated with damage or injuries to other people or property if you’re at fault in an accident.

- Personal Accident Insurance (PAI): This covers medical costs for you and your passengers if you’re involved in an accident.

- Personal Effects Coverage (PEC): This coverage protects personal belongings that are stolen from the rental car.

- Roadside Assistance: Some rental car companies offer roadside assistance coverage for emergencies such as a flat tire, lockouts, and towing.

It’s important to remember that these coverage options can vary depending on the rental car company and the country in which you’re renting. Additionally, you may already have some of these coverage types through your personal auto insurance policy or credit card benefits. Always read the terms and conditions carefully and check with your own insurance provider or credit card company before opting for additional rental car coverage.

Importance and benefits of having rental car coverage

Having rental car coverage can provide several key benefits and serve as an important safeguard in certain circumstances. Here are a few reasons why it’s crucial:

- Financial Protection: In the event of an accident or theft, having rental car insurance can save you from having to pay out of pocket for repair or replacement costs.

- Peace of Mind: Knowing you’re covered can make your rental experience more relaxing and enjoyable. You won’t have to worry about potential accidents or incidents impacting your finances.

- Personal Effects Coverage: If your personal belongings are stolen from the rental vehicle, rental car insurance can provide coverage, which your regular auto insurance might not offer.

- Gap Coverage: Rental car companies may charge fees for “loss of use” (when the car can’t be rented out while it’s being repaired) and diminished value (the reduction in a vehicle’s value after an accident). Many regular insurance policies don’t cover these charges, but some rental car insurance does.

Remember, before purchasing rental car insurance, it’s important to check your existing auto insurance policy and any coverage provided by your credit card company to avoid buying unnecessary coverage. It’s also crucial to understand the details of any rental car coverage you consider, as policies and protections can vary widely.

AAA’s Rental Car Insurance Policies

AAA provides its members with an assortment of insurance options, including auto insurance that extends to rental cars under certain conditions. Here’s a general overview of how AAA’s rental car insurance works:

- Extension of Personal Auto Policy: If you have a personal auto insurance policy with AAA, the coverage you have for your personal vehicle typically extends to rental cars. For example, if you have liability coverage, collision coverage, and comprehensive coverage on your personal vehicle, these will usually apply to the rental car, according to your specific policy’s terms and conditions.

- Rental Car Reimbursement Coverage: AAA offers rental car reimbursement as an optional coverage. If your insured vehicle is in the shop for covered repairs, this coverage can help pay for the cost of a rental car. However, this coverage doesn’t apply if you’re renting a car for vacation or other personal use.

- International Rental Coverage: If you’re planning to rent a car outside the United States, it’s essential to contact AAA directly to understand how your coverage may or may not apply.

- Possible Exclusions and Limitations: As with any insurance policy, there may be exclusions and limitations. For instance, AAA’s coverage might not extend to rental cars used for commercial purposes or ride-sharing services. Plus, certain fees that may be charged by the rental company, like “loss of use” fees, might not be covered.

- Claim Process: If an accident occurs while driving a rental car, you would typically file a claim with AAA in the same way you would for an incident involving your own vehicle.

- Rental Car Benefits Through AAA Membership: Depending on the tier of AAA membership you have, you may also be entitled to additional rental car benefits. These benefits could include discounts on rental car bookings, free rental days, or even enhanced coverage options, among other things. Different membership levels in the AAA provide different levels of services. Membership may cost between $60 and $100 with a sliding scale of inclusions. AAA members can receive discounts on rental cars at:

Other perks include:

- 24/7 roadside assistance including towing, winching, fuel delivery, and lockout service

- free child safety seat

- no additional driver fee

- no young driver fee

- discounts on flights, hotels, cruises and more

Please note, the specifics of your coverage can vary depending on the details of your individual policy and local AAA club, so it’s always best to directly contact AAA or check their official website for the most accurate and up-to-date information.

10 Reasons to Consider CarInsuRent Car Rental Excess Insurance

- Zero Deductible – In the event of an accident, you do not want to pay the deductible. Your rental car would also be subject to the high deductible on your auto insurance. Paying for car rental excess insurance and knowing you won’t be responsible for more than that amount may give you piece of mind.

- Make no claim on your personal insurance. Perhaps you’ve had a claim recently and don’t want your premium to skyrocket. You might want to err on the side of caution and purchase insurance because filing two claims in a single year will dramatically increase your insurance costs.

- Coverage in Foreign Countries: If you’re traveling internationally, your personal auto insurance policy may not provide coverage. Rental car insurance ensures you’re covered in these situations.

- Theft Protection: If the rental car is stolen, rental car insurance could cover the cost of the stolen vehicle.

- Protection Against Vandalism: Car rental insurance can cover the cost of repairs if the car is vandalized.

- Gap Coverage: Car rental companies may charge fees for “loss of use” and diminished value if their car gets damaged. These charges might not be covered by your regular insurance, but can be covered by rental car insurance.

- Personal Effects Coverage: This covers the theft of personal items from the rental car.

- Convenience and Peace of Mind: By opting for car rental insurance, you can avoid dealing with your own insurance company, and you don’t have to worry about your premiums increasing in case of an accident.

- Coverage in Case of Insufficient Personal Auto Insurance: If your personal auto insurance has a high deductible or low limits, rental car insurance can provide additional protection. If you are renting a pricey car, keep in mind that the amount of coverage provided by your Geico auto insurance is limited to the policy’s maximum. For your enjoyable Corvette rental weekend, you might want to increase your coverage. Check your coverage limits frequently.

- Coverage for Additional Drivers: If you plan to share the driving responsibilities with someone else during your rental period, rental insurance can ensure that all drivers are covered.

Amazing service. always efficient, friendly, responsive. i got my payment within days of submission. Bill is warm. A pleasure to work with them. highly recommended. I feel safe with them.

See How Much You Can Save on Your Car Rental Insurance

Get Started

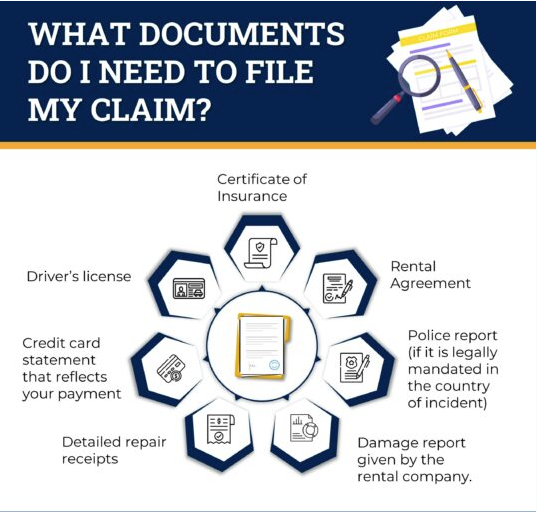

What Documents Do I Need to File My Claim?

It is important to research and understand the coverage options and costs to make an informed decision that best fits your needs. CarInsuRent car hire excess insurance starts from as low as $6.49 per day* to $94.90 for an annual car hire excess insurance policy. Our policies covers the excess on damage and theft up to €2,500 and provide full protection that Includes single vehicle damage, roof and undercarriage damage, auto glass and widescreen damage, towing expenses, misfuelling, loss of car key and tire damage. We cover multiple drivers between the ages of 21 and 84 years.

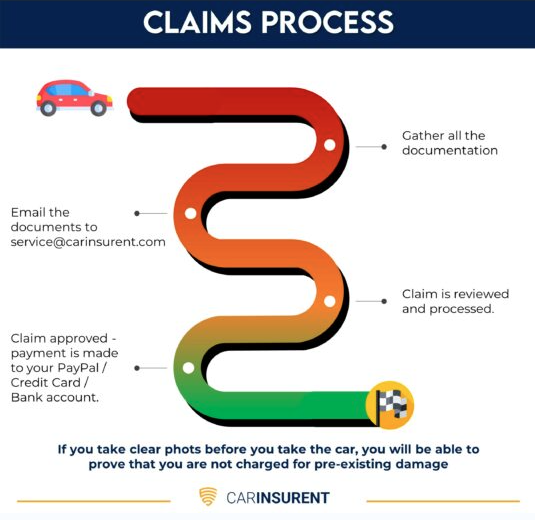

Claims Process

FAQ

Does AAA Auto Insurance Cover Rental Cars?

AAA Membership Does Not Include Car Rental Insurance. However, AAA auto insurance typically extends to rental cars, but the specifics can depend on the terms and conditions of your individual policy.

Only AAA members can buy AAA auto insurance. You are normally protected for rental cars with AAA auto insurance up to your similar policy levels in the United States. You might not have enough coverage if you drive an old beater at home but hire a brand-new premium vehicle. The best course of action is to review your policy and call AAA to confirm your coverage limits before you arrive at the rental desk. In some circumstances, you might want to get extra insurance from CarInsuRent.

Travel Tips and Guides

Frequently Asked Questions (FAQ)

Can I buy a plan for just one day?

Can I buy a plan for part of my rental only?

No. We provide a single journey plan. You are covered from the time you pick up the rental car up to the time you return it or on the last date written on your Certificate of Insurance, whichever comes first.

Can I buy a plan when I pick up my rental car?

No. You should purchase a policy before starting your travel.

Find the answers you’re looking for to the most frequently asked car hire insurance questions as well as other questions relating to our products and services.